Community

American Heart Association: CycleNation 2026

Read more

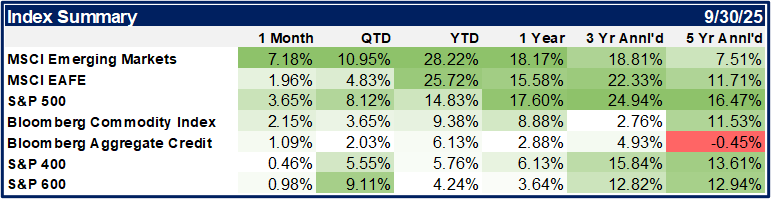

The stock market rally that began after the tariff tantrum in April picked up momentum during the 3rd quarter. An improvement in leading economic indicators and softer labor market data created cross-current conditions for the Federal Reserve to consider but ultimately resulted in the Fed lowering its benchmark interest rate in September. Against this backdrop, the S&P 500 recorded 23 new all-time closing highs, rising 8.1% during the quarter and increasing its year-to-date gain to 14.8%.

The decline in interest rates, and broader policy shift, acted as a catalyst for broader market participation as the S&P 400 Mid Cap Index posted a gain of 5.5% during the quarter, bringing its year-to-date return to 5.76%. The more rate-sensitive S&P 600 Small Cap Index outperformed its larger market-capitalized peer indices, achieving a return of 9.1% and reaching positive territory for the year with an overall return of 4.2%.

Source: YCharts

International equities continued to deliver compelling relative returns. The MSCI EAFE Index rose by 4.8% during the quarter and achieved a gain of 25.7% for the year. Emerging market stocks also outperformed, climbing 10.9% in the quarter and 28.2% year-to-date.

The Federal Reserve’s first rate cut since December 2024 contributed to a decline in 10-year Treasury yields, moving from 4.22% at the beginning of the quarter to 4.15% by the end. This drop in yields, combined with tightening credit spreads, supported gains in the Bloomberg Government/Credit Index of 1.5% for the quarter and 5.7% for the year. Similarly, the yield environment provided a tailwind for municipal bonds, as the Bloomberg Municipal 1-10 Year Index rose 2.3% and 4.1% during the same periods. Gold maintained its historic pace of growth, rising 16.7% during the quarter and further enhancing its appeal during this period in which it rose nearly 50% year-to-date.

Since the launch of ChatGPT in November 2022, the influence of AI-related stocks on the market has been extraordinary. These companies have contributed 75% of the S&P 500’s total returns, driven 80% of the index’s earnings growth, and been responsible for 90% of the capital spending since that time. This remarkable concentration of performance and capital investment highlights the transformative role artificial intelligence is playing in shaping the economy and market dynamics.

As the large-cap posterchild of the AI boom, and proverbial supplier of pickaxes to the gold rush, Nvidia’s stock has been dominant over the last three years. The company’s stock price soared by an impressive 1,280% from November 1, 2022, to September 30, 2025, fueling an 81% gain in the S&P 500. In comparison, an equal-weighted S&P 500 index advanced only 43% over the same period. This stark disparity highlights the difficulty diversified portfolios face in outperforming a market dominated by a handful of leading stocks, reminiscent of the late 1990s when market breadth was limited to a similarly small cohort of companies.

As a result of this surge in AI leadership, the valuations of the largest public technology companies—including Nvidia, Amazon, Apple, Meta Platforms, Microsoft, and Tesla—have risen sharply. That group now trades at a 47x multiple on its last twelve months of earnings. In comparison, the S&P 500 (which is currently quite expensive relative to its own history going back to the Dot Com Bubble) trades at a 28x multiple of its prior earnings.

Source: Factset

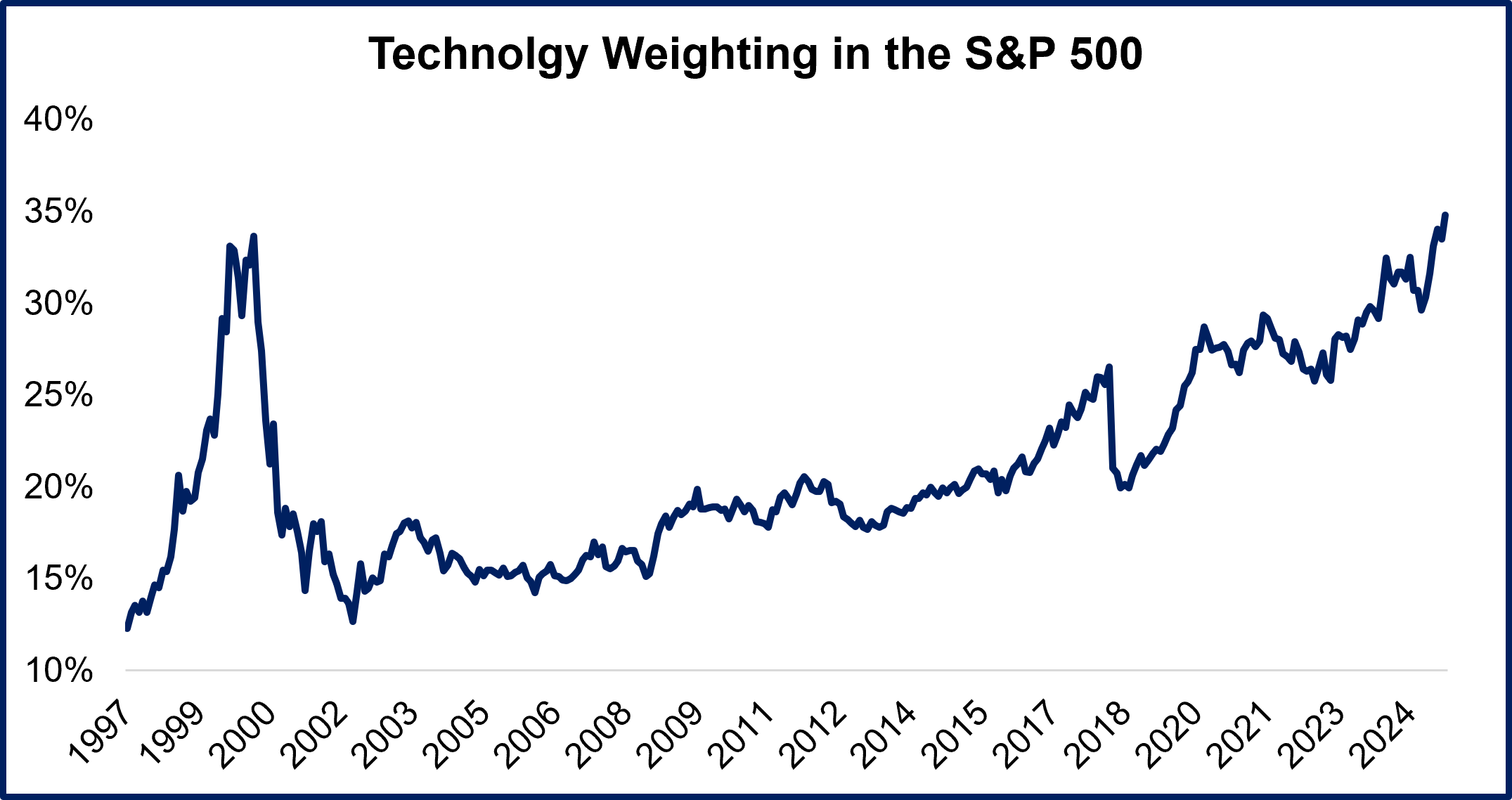

These firms now command a significant share of the market, illustrated in the chart above, reflecting significant investor enthusiasm for both their growth prospects and their integral role in AI development. The technology sector’s weighting within the S&P 500 has now returned to levels not seen since the peak of the technology bubble.

To be fair, while we draw similarities between these periods, there are important differences in how this leadership evolved. During the late 1990s, technology’s ascent within the index occurred rapidly, fueled by speculative fervor. In contrast, the current rise has been more gradual, taking over a decade of sustained leadership and consistent performance for the sector to reach its present prominence. This trend has been supported in part because the technology companies leading the market today are financially more robust than those of the past.

Many of today’s leaders have generally managed less leveraged balance sheets, reduced cyclicality, strong free cash flow generation, and substantial competitive advantages. While these attributes have directly influenced their higher valuations, it remains essential to acknowledge that such elevated valuations also reflect a certain level of investor exuberance and allow for minimal margin of error.

Revenue growth has certainly been central to the AI-driven craze driving the tech sector, and specifically mega-cap stocks (often referred to as “hyperscalers”), higher. We recognize the impressive nature of these growth stories, and they should not necessarily come as a surprise given the technological advancement that is unfolding. However, our investment principles prompt us to carefully evaluate both the source and methods of revenue generation, as well as the sustainability of their growth stories. At the end of the day, these companies need to prove out widescale adoption and profitable use cases for what has been spent thus far in the AI infrastructure buildout.

In the 1989 film “Field of Dreams”, the protagonist played by Kevin Costner hears “if you build it, he will come” whispered to him as he walks through his corn field. If you have seen the film, you know that Costner’s character goes on to level his field of crops in order to build a baseball field in hopes that “Shoeless Joe” Jackson and other legendary baseball players will show up to play. The potential negative financial ramifications of that decision are

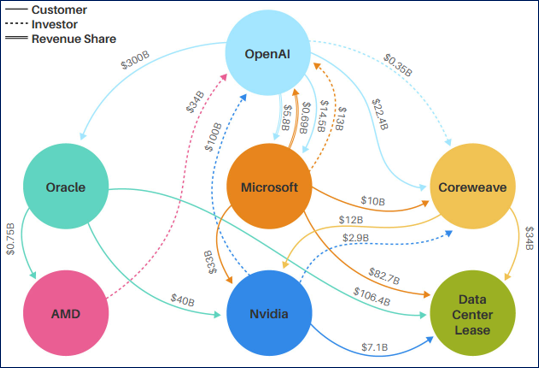

implied throughout the film, and even the character’s own family members began doubting his sanity. Ultimately, the players arrive in what is the movie’s grand payoff, but what if they had not? That hopefulness of a future payoff echoes in our minds when we hear terms like “arms race” or “CapEx boom” in relation to AI and machine learning. We have to question who is truly footing the bill for the anticipated revenue and earnings growth presumed to result from these extraordinary capital outlays. It appears that rapid growth is being, at least in part, subsidized by a “passing of the hat” amongst the hyperscalers, where spending and indirect investment in each other has helped support the growth story. A graphic from a recent Barron’s article depicting some of this circularity can be seen below.

Source: Morgan Stanley, Barron's

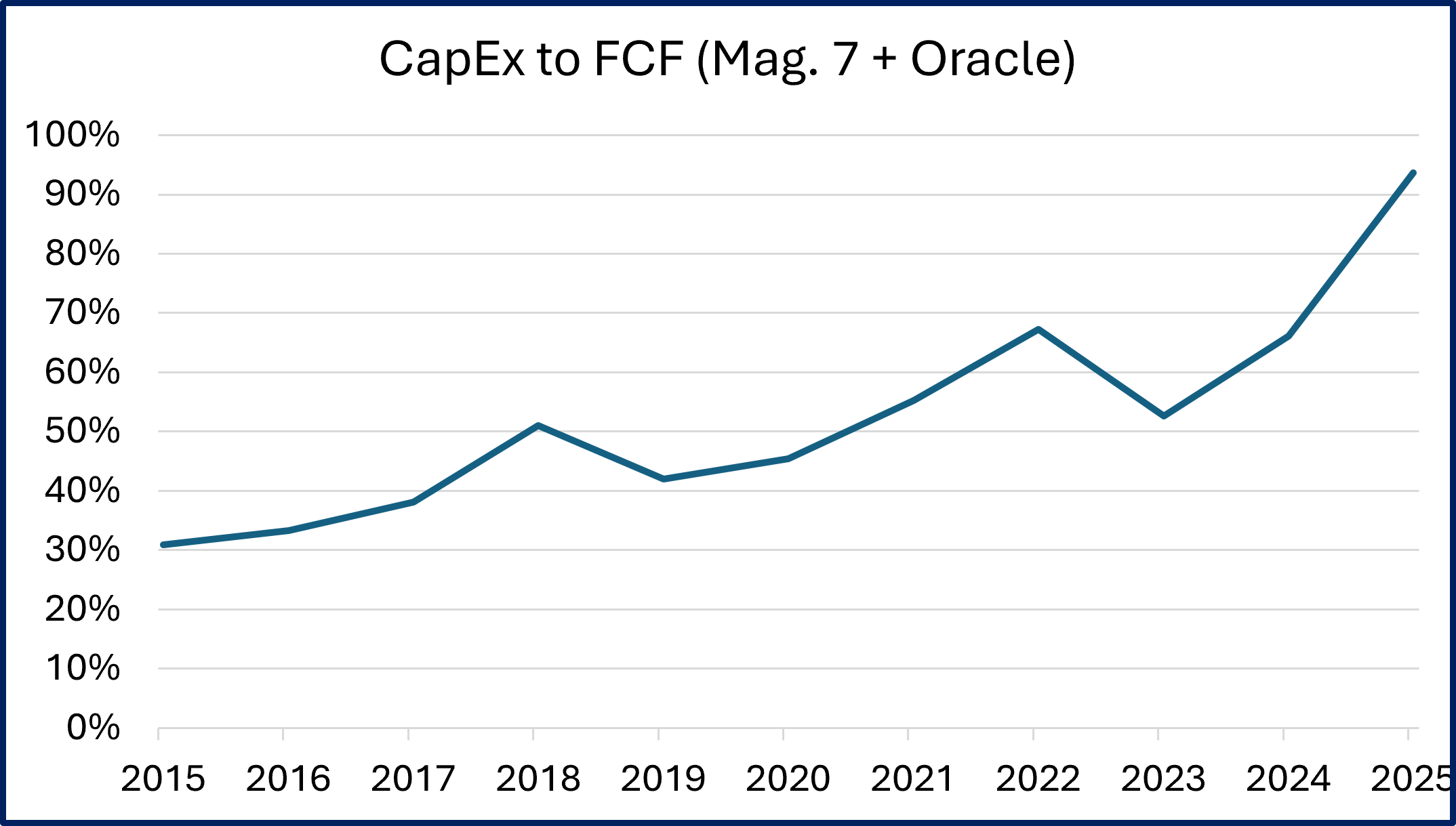

Capital expenditures as a percentage of free cash flow among the hyperscalers (Nvidia, Apple, Amazon, Microsoft, Google, Meta, Tesla & Oracle), have risen dramatically over the course of the last decade while the tech sector grew as a component of the broader market. As seen below, those capital expenditures have grown from just over 30% of free cash flow to over 90% of free cash flow. So far, most of the group has had the cash generating capacity to fuel the spending spree without taking on debt, but current spending growth rates do not appear sustainable.

Source: Factset

Some questions we must ask:

As these questions are considered, it is important to acknowledge the inherent difficulty in making accurate forecasts, particularly regarding the wide-ranging impact artificial intelligence may have on the stock market and the U.S. economy. In the face of uncertainty, relying on principled investing—allocating capital based on reasonable assumptions related to earnings, cash flow, and value—remains a sound approach.

Price matters. This section’s title phrase was coined by a Resonant-favorite investor and author Howard Marks, who has written for decades about maintaining discipline when markets are tipped heavily by the natural human emotions of fear and greed. The valuation of assets upon purchase plays a critical role in shaping forward returns. Currently, the top eight stocks in the market are trading at a price-to-earnings ratio of 40x, which is notably higher than historical norms. For comparison, ten years ago these stocks traded at 17x earnings, while the remainder of the market was valued at 19x earnings.

The future direction of the current market cycle remains uncertain; however, history has shown that periods when investors are willing to pay almost any price for exposure to certain stocks have typically ended unfavorably. This pattern serves as a reminder to maintain caution and discipline in investment decisions.

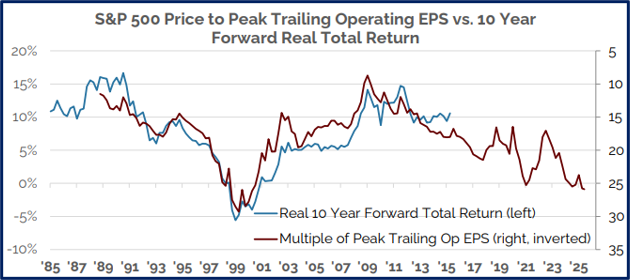

While valuation should not be used as a precise timing instrument for market participation in the near term, it does reflect the assumptions and expectations embedded in current market prices. The price paid for a security has a direct impact on its prospective returns over longer periods of time.

Source: Distillate Capital

As illustrated in the chart above, there is an inverse relationship between valuations and forward returns: as valuations rise (moving lower on the right axis), expected forward returns tend to decrease (moving lower on the left axis). If this trend were to hold, elevated current valuations are signaling the likelihood of lower returns for domestic large-cap stocks over the next decade. In light of this, investors may be looking elsewhere for return potential.

Elsewhere in the investment landscape, gold has been on a terrific run, posting a nearly-50% return year-to-date. This is somewhat of an odd dynamic as “safety” plays like gold typically do not make significant runs during booming periods in the stock market. For many years, gold has been widely regarded as a protective asset, especially during periods characterized by low interest rates, elevated equity valuations, a declining dollar, heightened trade and economic uncertainty, and expanding deficits. Investors have often turned to gold as a hedge within their portfolios, relying on its perceived stability in times of market turbulence.

Gold prices have steadily increased over the past three years, independent of shifts in economic or political conditions. Rather than experiencing a conventional rally, gold may be undergoing a phase change in its role within global markets.

On one hand, domestic fiscal and monetary policies are contributing to reduced confidence in the US Dollar while simultaneously increasing the appeal of gold as an investment. Reduced confidence stems from expanding budget deficits and a mounting national debt. Importantly, there is little political motivation to pursue fiscal restraint.

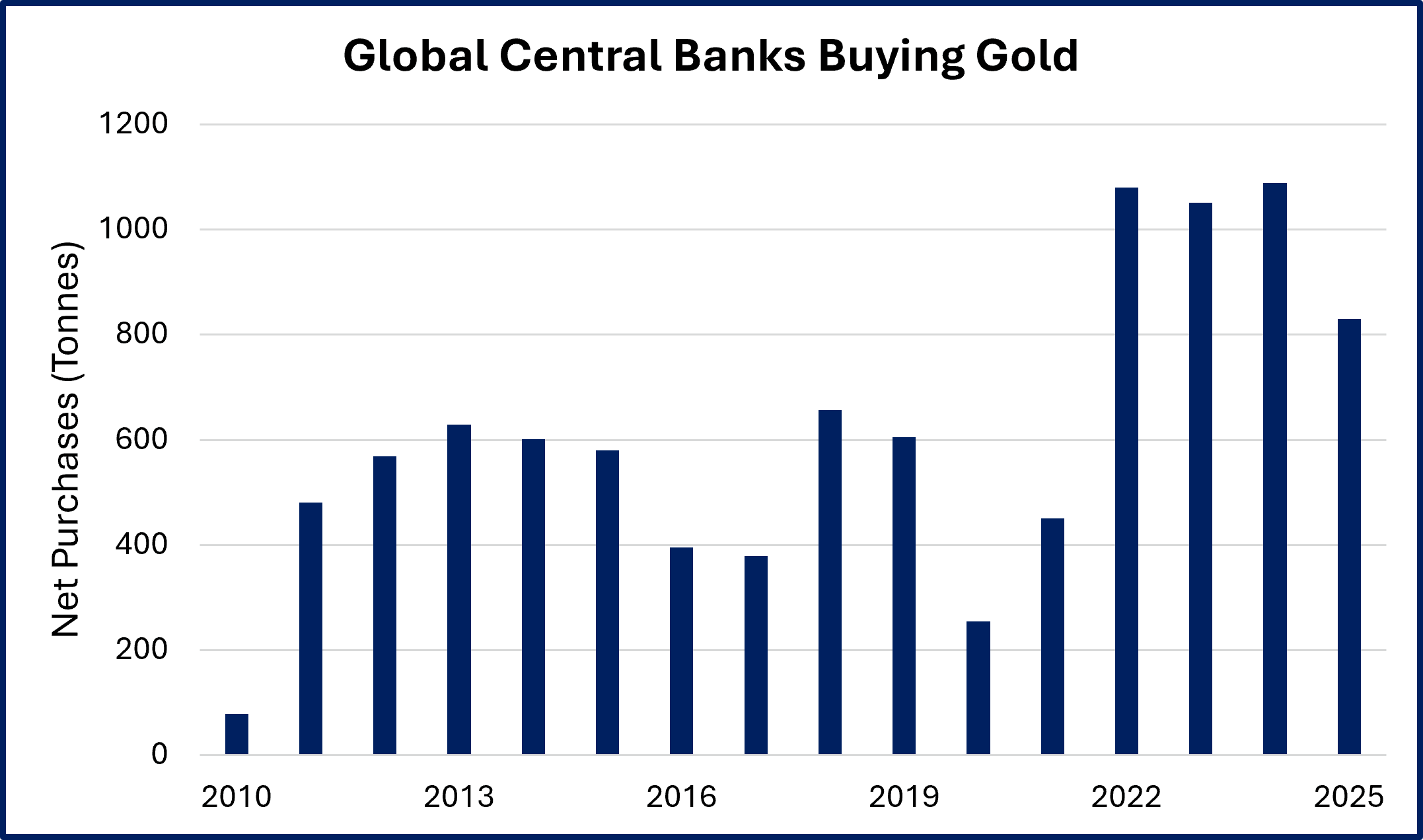

Simultaneously, International investors appear to be shifting their assets away from US Treasuries, aiming to decrease their reliance on the dollar and limit their exposure to risks tied to the US. Global central banks are increasing their gold acquisitions, indicating a potential shift in reserve management strategies and asset allocation. The World Gold Council reports that global central banks bought an average of 600 tonnes of gold per year from 2010 to 2021. This figure rose sharply to over 1,000 tonnes annually between 2022 and 2024.

Source: World Gold Council, MacroMicro

It leaves us wondering if a global macroeconomic shift might be underway in which the US dollar wouldn't be replaced as the reserve currency but could become part of a multi- currency pricing system, where final settlements are made in gold at a rate that adjusts according to all currencies. We will continue to explore this idea and its potential impact on investment portfolios.

Meanwhile, we are not the only ones astonished by gold’s recent price movements. It has also caught the attention of investors, including Ken Griffin, the billionaire founder of Citadel. He remarked, “Investors are not just flocking to gold; they're also turning to alternative assets like Bitcoin. It's surprising to see, and it's concerning that people now regard gold as a safe haven in the same way they used to view the dollar.”

While much attention remains focused on the market’s largest companies, we continue to find compelling investment opportunities across the broader market. Notably, smaller stocks have historically delivered superior long-term performance compared to their larger counterparts. This historical outperformance underscores the importance of maintaining a diversified approach and not concentrating solely on the biggest names.

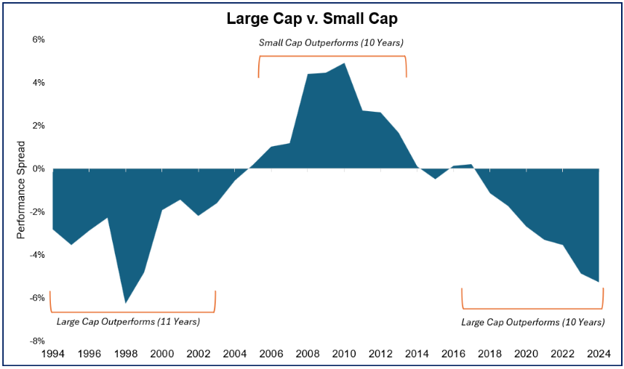

For some time, higher-for-longer interest rates posed a significant headwind to small cap stocks, dampening their performance relative to larger firms. However, the recent decline in interest rates has provided a catalyst for small cap equities, fueling a notable rally over the past quarter.

The recent period of underperformance for smaller stocks has reached extremes in terms of relative performance. Historically, such extremes have often been followed by a powerful reversion to the mean, suggesting the potential for a strong rebound in small cap equities.

Source: Factset

Amid the excitement and enthusiasm surrounding the artificial intelligence (AI) sector, remaining committed to a diversified approach that includes exposure to mid and small caps has required patience, discipline, and a willingness to take a contrarian stance. While the momentum in AI-related stocks has been significant, we recognize the long-term opportunity in staying committed to relative value despite short-term volatility.

We are encouraged by recent market activity, particularly the outperformance of the S&P 600 relative to the S&P 500 in the third quarter. This may represent the beginning of a new cycle in which smaller stocks regain leadership, offering renewed opportunities for investors seeking growth beyond the largest market constituents.

The saying “the market climbs a wall of worry” is a familiar one in financial circles. It highlights an important market phenomenon: even in the face of persistent concerns, negative headlines, or uncertainty, markets have historically tended to rise over time. This resilience demonstrates that some degree of worry is a natural and even necessary part of a healthy market environment.

A measured amount of concern serves a valuable purpose for investors. When fear is absent, complacency can set in, increasing the risk of overconfidence and encouraging riskier behavior among investors. This environment can contribute to the formation of asset bubbles or unsustainable trends.

Currently, several positive factors are supporting the markets: stock indices are reaching record highs, interest rates are declining, and high yield credit spreads are lingering near historically low levels. Tax cuts are on the horizon, which could further boost corporate profits. The broader economy has displayed resilience, recession fears have eased, and tariffs have so far had little tangible effect on profit margins or inflation.

Amid these positives, enthusiasm for artificial intelligence (AI) and ongoing monetary policy easing are capturing much of the market’s attention. These factors are, for now, overshadowing concerns about tariffs and signs of weakness in the labor market.

Yet, the lack of widespread worry in the current environment gives us pause. A market characterized by minimal concern can be vulnerable to unexpected shocks, especially when starting with historically high valuations. In recognition of this, we continue to maintain a diversified approach—investing in segments of the stock market that present attractive valuations, while also balancing portfolios with high-quality, intermediate-duration fixed income securities.