Community

American Heart Association: CycleNation 2026

Read more

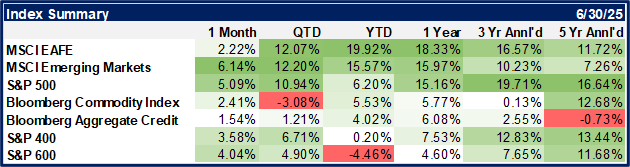

Stocks shrugged off trade war-induced volatility, global conflicts (including the U.S. bombing Iran nuclear sites) and domestic policy uncertainty during the second quarter of 2025 to produce robust returns. The S&P 500 Index advanced 10.9%, bringing its six-month total return to 6.2%. Medium and small-sized companies also participated in the rally: the S&P 400 Midcap 400 returned 8.1% and the S&P 600 SmallCap 600 rose 8.5%. This brought their respective year-to-date returns to 3.9% and -1.8% respectively. Internationally, returns were even better, as the developed markets MSCI Europe, Australasia and Far East (EAFE) index advanced 12.1% to bring its six-month return to 19.9%. The MSCI Emerging Markets Index rose 12.2%, bringing the year-to-date return to 15.6%.

The yield on the benchmark 10-year maturity Treasury bond ended marginally higher. It began the quarter at 4.21% and ended at 4.23% after rising to 4.60% in late May. The Bloomberg Intermediate Government Credit Index rose 1.7% during the quarter, bringing its six-month return to +4.1%. Municipal bonds did not fare nearly as well: The Bloomberg 1 -10 Year Municipal Bond Index declined -.1% during the quarter and remains at a loss of -.4% on the year.

Source: YCharts

President Trump made tariffs a central theme of his 2024 campaign. Plans to implement them dominated market activity during the quarter. The S&P 500 was already down -8% on tariff-related concerns prior to Trump’s “Liberation Day” announcement on April 2nd. Investors had not expected the size and scale of what he announced, particularly a 145% levy on Chinese goods. Consequently, the S&P 500 underwent a rapid correction, declining by -10.5% over a two-day period, while the CBOE Volatility Index (VIX) surpassed 50—a level reached only twice in the past three decades. The extreme market volatility led Trump to then pause the tariffs on April 9th, restoring investor confidence and resulting in a remarkable S&P 500 mid-day surge of 9.5%. The pause marked the peak for trade policy uncertainty and despite ongoing geopolitical tensions the S&P 500 ended the quarter near an all-time high.

Solid macroeconomic fundamentals further underpinned this recovery. Consumer spending remained steady, growing at an annual rate of 1.7%. The labor market also showed continued resilience. The unemployment rate is holding at 4.2%—well below its historical average—as companies prioritize talent retention. Furthermore, inflation has continued its downward trajectory. May’s Consumer Price Index report surprised to the downside, with headline inflation at 2.4%, edging closer to the Federal Reserve’s 2.0% target. Collectively, the improvement in these fundamentals has bolstered hopes for a more accommodative Fed.

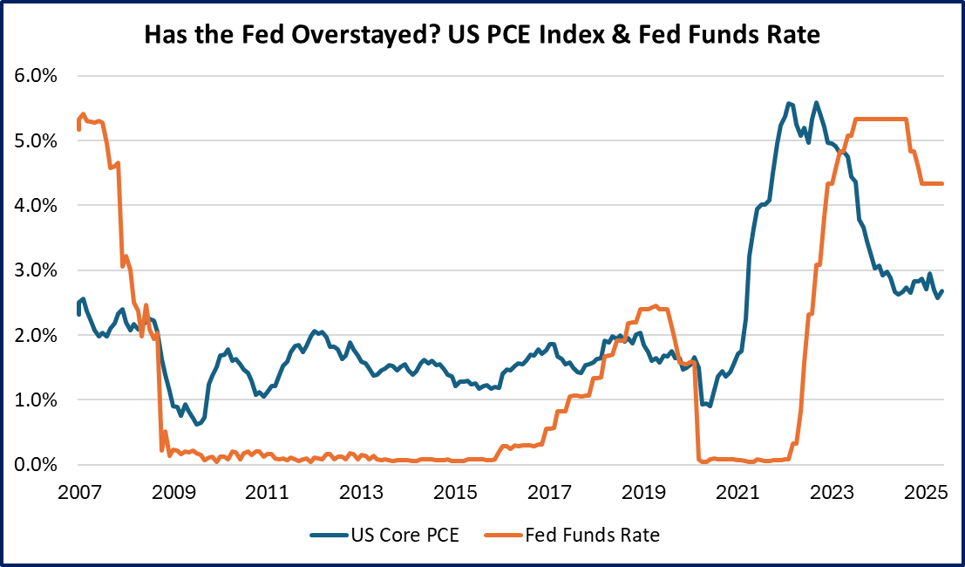

International indexes have outperformed U.S. markets this year. Structural reforms in the European Union, especially in Germany, have increased public investment and defense spending in response to U.S. trade policy shifts. The European Central Bank has cut its key rate to combat inflation and support growth, while our Federal Reserve remains cautious. Fed Chair Powell has held rates steady despite pressure from the Trump Administration to lower them, as the Fed assesses the economic effects of tariffs. There is a risk that the Fed stays too restrictive for too long, as seen in previous instances where prolonged tight monetary policy contributed to economic downturns. As reflected below, the current gap between inflation (illustrated by the Fed’s inflation gauge of choice: the Personal Consumption Expenditures Index, or “PCE”) and the federal funds rate is the largest since 2007, which preceded the Great Financial Collapse of 2008.

Source: YCharts

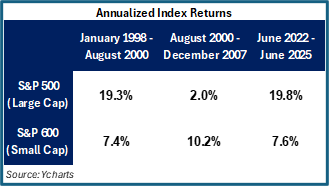

A change in Fed policy could be a catalyst for a broadening of market leadership beyond large company stocks. The return differential between large and small company stocks has become historically wide. For the 3-year period ending on June 30, 2025, the large cap S&P 500 had an

annual return of 19.8% compared to the small cap S&P 600’s annualized return of 7.6%. It is not unusual for small company stocks to experience prolonged periods of underperformance before rebounding. For example, in the run up to the technology bubble collapse of 2000, small company stocks also underperformed by a wide margin only to outperform over the ensuing eight years, which is displayed in the above table.

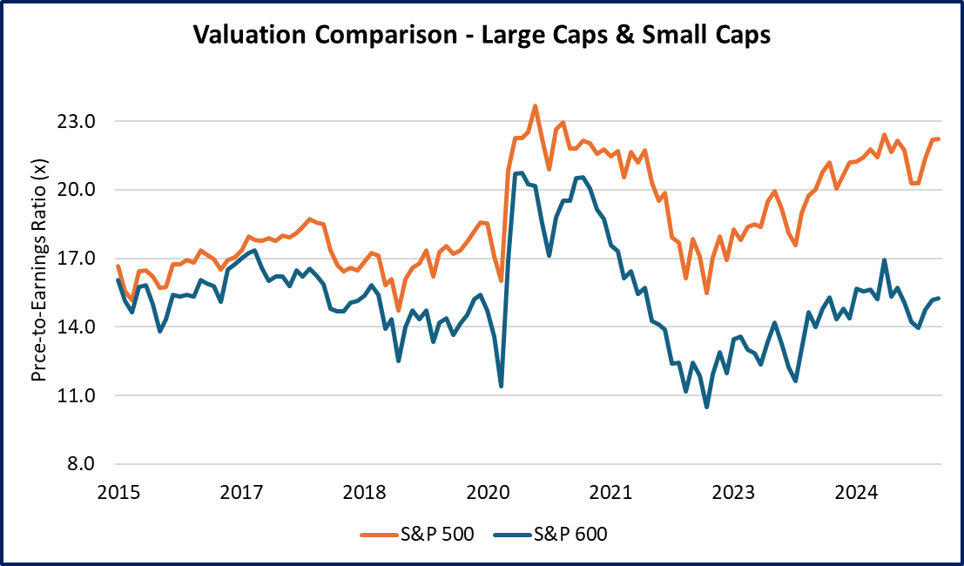

Trends can last longer than we expect, but the recent return differential may be setting up a mean reversion opportunity between large and small company equities. Further, small company stocks are trading at an attractive discount to large companies due to recent market volatility and investor caution, as can be seen in the chart below.

Source: Factset

Timing a shift in leadership is challenging and valuation alone is not always an effective timing tool. However, the disparity in both performance and valuation is too large to ignore. As long-term investors we seek to diversify portfolios and take advantage of valuation discounts. We may have to wait a bit longer, but historically when the Fed cuts rates, it reduces the cost of capital. This is particularly helpful to small-sized companies and could spark a rotation of investor interest toward an area of the market that has been unloved for several years.

In the past quarter the markets have digested a number of significant developments: the Liberation Day tariff announcement and subsequent market pullback, ongoing trade policy uncertainty, mounting concerns related to size of the fiscal debt, geopolitical tensions between Israel and Iran, a greater than 30% spike in oil prices, and a US military strike in Iran. Despite this, the stock market has been extremely resilient in reaching new highs.

A favorite movie scene comes to mind from the classic police comedy, The Naked Gun. In the film, Leslie Nielsen’s character, Lt. Frank Drebin, tries to control a chaotic crime scene after a car chase ends with a suspect crashing into a fireworks factory. As he tells onlookers to disperse by telling them there is “nothing to see here”

fireworks explode behind him as people jump from the burning building. In a similar vein, the markets appear to be ignoring both domestic and geopolitical risks. Rather than taking the cavalier attitude of Lt. Drebin, we will remain vigilant in analyzing current market conditions while maintaining our focus on implementing enduring investment strategies. We manage risk through global diversification, disciplined portfolio construction, and a commitment to high-quality, long-term investments. Importantly, we are stewards of your capital and will help you navigate any uncertainty with confidence and composure.