Community

American Heart Association: CycleNation 2026

Read more

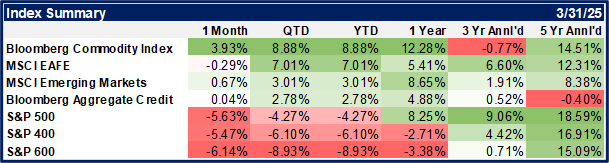

U.S. equities faced a challenging first quarter, with the large capitalization S&P 500 (-4.27%) experiencing its worst performance since the third quarter of 2022. The NASDAQ large company growth index (-10.26%) and Russell 2000 SmallCap (-9.48%) also posted their steepest declines since the second quarter of 2022. Markets started the year strong, with the S&P 500 hitting a record high in February before growth concerns, AI skepticism, and trade policy uncertainty fueled a sharp selloff and moved the index into correction territory. The “Magnificent 7” became the “Lag-nificent 7” as this group of stocks fell an average of -25% from their 52-week highs, making up 96% of the S&P 500’s year-to-date decline. Global equities, on the other hand, outperformed their U.S. counterparts as fiscal stimulus caught investors’ attention and ignited a very cheap market. The MSCI EAFE Index of developed international equities produced a 7.01% return in the first quarter, and the MSCI Emerging Markets Index generated a total return of +3.01%.

Bond investors were rewarded as yields fell during the quarter, despite the Federal Reserve staying on the sidelines. The 10-year Treasury yield dropped to 4.21% on March 31st from 4.57% on December 31st. The decrease in yield drove the Bloomberg Intermediate Government/Credit Index to a +2.42% gain. Tax-exempt bond yields followed a similar but slightly more-muted path than their taxable counterparts, as the Bloomberg Municipal 1-10 Year Index eked out a +0.70% total return.

Source: YCharts

Following two years of strong market performance and relative stability, the first quarter of 2025 marked a significant shift in investor sentiment. The reemergence of trade tensions under President Donald Trump redirected the market’s focus from continued expectations of a “soft landing” for the economy and potential Federal Reserve rate cuts. Instead, investors pivoted to renewed (and heightened) concerns about a trade war reviving upward pressure on inflation, collapsing consumer confidence, and increased recession risk. These developments triggered a series of market rotations, notably into value-oriented and international equities.

Over the past two years, growth stocks—particularly mega-cap technology names—have dominated market headlines. The so-called “Magnificent Seven” (Alphabet, Amazon, Apple, Meta, Microsoft, Nvidia, and Tesla), along with other prominent tech firms, propelled equity markets to record highs amid investor enthusiasm surrounding artificial intelligence (AI) and expectations of robust earnings growth. However, more recently, these mega-cap tech stocks have come under pressure due to concerns over elevated valuations and the sustainability of their earnings trajectories. At the same time, market breadth has improved, allowing more economically sensitive and value-oriented sectors—such as financials, energy, and industrials—to gain momentum and, in some cases, outperform the former darlings of Wall Street. We’ve written consistently and extensively about our view that the Mag 7 dynamic was unsustainable, and unfortunately those predictions came to fruition in the first quarter of 2025.

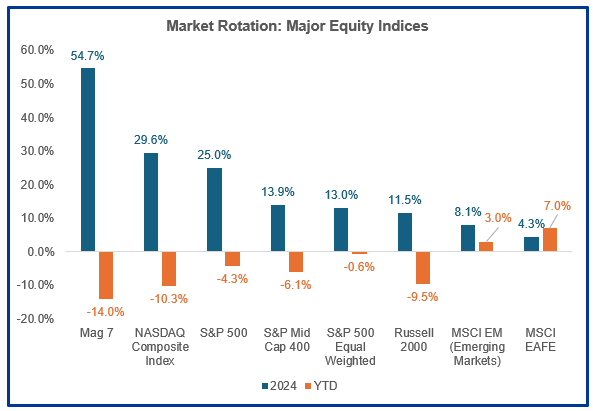

But investors didn’t pivot simply to U.S. value stocks; the market rotation went global. After a long stretch of underperformance, international equities made a comeback in Q1’25, which you can see in the chart below. The MSCI EAFE’s +7.01% return over the first quarter significantly outperformed the U.S. market. The prevailing wisdom for the last decade has been that the “the United States innovates, China imitates, and Europe regulates.” The trailing return for the prior ten years ending March 21st, 2025, for the S&P 500 was 226% while the MSCI EAFE index registered a return of 72.6%. That trend, at least in investor sentiment and momentum, reversed in the first quarter.

We have always paid close attention to mean reversion when considering asset class positioning in client portfolios. Is the period of American exceptionalism over? We do not think so, but we do recognize that the S&P 500 trades at premium relative to the MSCI EAFE index. Investments can remain cheap for a long time and returns might still lag, absent a catalyst to generate higher valuations. We do believe the catalyst could come from any of: 1. increased fiscal spending by European countries; 2. an end to the hostilities between Ukraine and Russia and/or; 3. a weakening of the U.S. dollar. The Trump administration policies have already prompted Europe to increase fiscal spending. Importantly, Germany—which accounts for 30% of the Eurozone’s GDP and has historically been fiscally conservative—led the start of the European fiscal stimulus with renewed defense spending, among other initiatives. Additionally, a softer dollar and historically low valuations have helped offset some of the tariff-related headwinds in international markets.

Source: FactSet

This year has been marked by heightened uncertainty, with tariffs emerging as a central concern. While tariffs themselves are not a new phenomenon, their erratic rollout and the lack of clear guidance have unsettled businesses, investors, and markets alike. Post-election market euphoria quickly gave way to uncertainty, which the President suggested would be clarified on April 2nd. Normally, removing uncertainty from the market helps propel risk assets higher. The opposite occurred as the announced tariffs’ size, scope and detail were well beyond what investors expected, which has led to a dramatic sell-off in equity-based assets. We believe tariffs are a tax on exporters, designed to raise revenue and strengthen or weaken certain participants. If you tax anything, you get less of it – in this case, less trade and less consumption due to higher prices. The administration seems to think this policy is acceptable in that Americans need fewer goods and the world needs less of both our products and our treasury bonds.

The White House is walking a tightrope if the policy aim is to slow the economy, compel the Fed to lower rates and thus produce higher levels of investment and growth. Contracted and less-open markets, slowing growth and shrinking poll numbers in advance of mid-term elections do not tend to be the stuff that successful policy, or politics, are made of. Our expectation is that we will see some combination of negotiated change and walked-back policy. In thinking about this recently, the family toast of an acquaintance came to mind. A part of their celebratory salutation, across generations, has been “May We Never Have Less.” We like to think of it as a reminder that they once did (have less), but also how much effort is required to be productive enough to advance any endeavor that creates excess capital – wealth that can be saved, invested, preserved, gifted – across longer periods of time, even generations. We hope that the Administration is mindful of their place in history, for if they deliver an American economy not marked by abundance but by contraction, or by constraint rather than mobility, that history will judge them exceedingly harshly.

Our objective is not to portray an overly pessimistic view of the macroeconomic landscape, but rather to present a clear-eyed assessment of the current environment. In unsteady times, we align our thinking with the perspective of Warren Buffett: doubt can serve as an ally to the long-term investor. Market dislocations and elevated fear often create compelling investment opportunities. At Resonant, we remain measured in our approach, focusing on policy developments rather than political noise and rely on tactical adjustments to diversified portfolio allocations seeking to increase probabilities of intermediate-to-longer term success. Markets are remarkable sorting mechanisms, and they both respond to and influence decision-makers in the vast multivariable ecosystem that makes up the global economic, policy and security structures.

In our view, continued pressure on the economy could ultimately prompt lower interest rates and the adoption of more pro-growth policies, though unintended consequences have and may continue to result. Until conditions improve, or at a minimum become more rational, we are addressing uncertainty through disciplined diversification. During periods of heightened volatility, it’s essential to remember that the strength of a portfolio lies in its construction. A well-diversified portfolio helps ensure that no single investment can meaningfully derail long-term financial progress.

Accordingly, we maintain broad exposure across asset classes, sectors, and geographic regions. Given the current trade environment and valuation levels, we have adopted a more cautious stance in our portfolio models—favoring high-quality, capital-preserving assets such as fixed income and cash. This positioning affords us the flexibility to re-enter risk assets when conditions become more favorable. But we do also look to take opportunistic risk when it is priced attractively – as an example, we increased our exposure to international equities in our models in the first quarter, seeking to capitalize on some of the relative attractiveness outlined above. And we are modeling an increase in U.S. equities, along with tactical adjustments to our factor weights, at the time of this writing.